In comparison to other metals, Tin reserves and production is relatively small. For instance, the world’s quantity of refined tin barely reached 1.4% of that of copper in 2020.

Nowadays, there are 338 tin deposits worldwide. Most of tin resources we currently know are in Asia. Altogether, China (39%) and Russia (11.7%) hold half of them1.

Its extraction depends on several factors, besides resource availability. Economic feasibility of tin reserves depends on its concentration and mine extraction cost, which is influenced by the international tin price. Therefore, some of the main producing countries do not necessarily have most known tin resources.

1 Global Resources & Reserves 2020 – International Tin Association.

Source: Mineral Commodity Summaries 2023 – US Geological Survey.

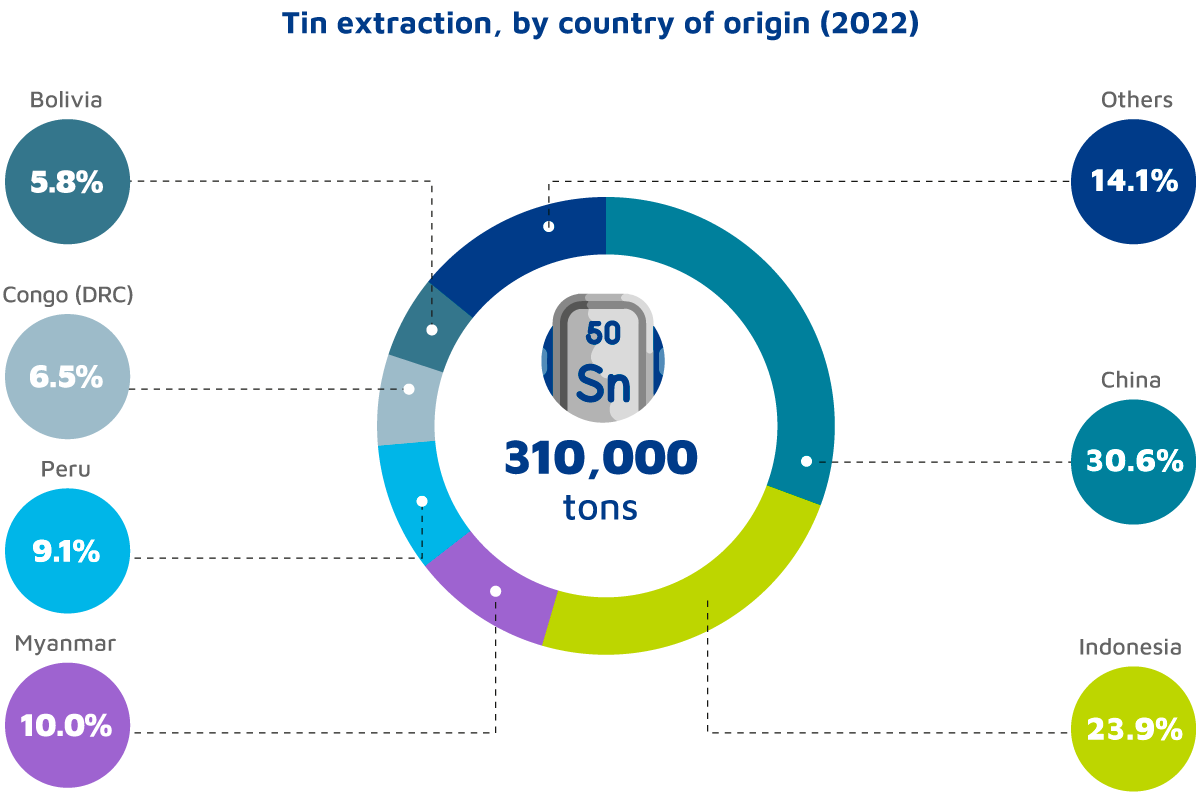

310,000 tons of tin were extracted in 2022. If we consider only the currently known resources, tin mining activities could only be sustained for another 50 years, if they continue at the same rate.

Additionally, tin is recyclable without losing its quality. Hence, 380,400 tons of global refined tin production in 2022 included approximately 70,400 tons of recycled tin. Only 5 companies accounted for 44.4% of total tin production.

*It includes Taboca, its subsidiary in Brazil. / Source: International Tin Association.

Minsur is the main producing company outside Asia and the second largest worldwide. San Rafael, its mining unit in Puno (Peru), is one of the world’s largest tin mines. It accounts for nearly 9% of tin extracted every year.